September Market & Economic Recap: The Fed's Easing Cycle Begins Against Backdrop of Cooling Employment

September proved to be an eventful month. After building anticipation, the Federal Reserve delivered its first rate cut of 2025, moving the target range to 4.00%–4.25%. Equity markets responded eagerly, reaching new highs, though signs of underlying tension emerged.

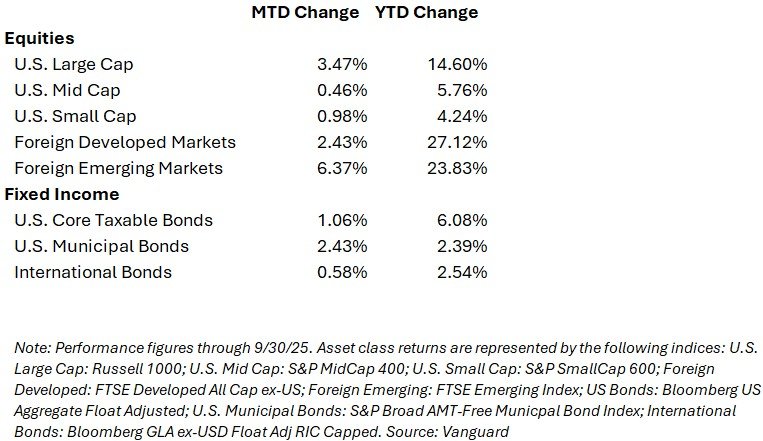

Market Performance

Equities – U.S. & Global

- U.S. equity markets extended their gains, with major indexes touching fresh all-time highs in part on the relief rally following the rate cut.

- Momentum and technology sectors outpaced broader indices, while small- and mid-caps also benefited from the lower-rate backdrop.

- On the international front, emerging markets and some developed ex-U.S. equities performed well, bolstered by weaker U.S. rates, favorable currency dynamics, and selective regional strength (notably in Asia)

Fixed Income & Credit

- The rate cut raised expectations for further easing this year, helping support bond prices and compressing yields.

- Credit spreads–the difference between yields on riskier bonds relative to low-risk bonds– tightened, reflecting improved investor risk appetite and confidence that lower policy rates would lift credit markets.

- However, pockets of stress emerged in sectors with heavy issuance, and municipal bond markets saw yield increases in places due to elevated supply.

Market Snapshot (through September 30, 2025)

- The “Fed put” notion–where the Fed will intervene to support financial markets during a significant market downturn–has resurfaced: markets still appear to lean on central bank support as a backstop.

- The rally hasn’t been without cracks:

- Narrow leadership: Gains have been concentrated in a handful of large-cap technology and momentum names. Breadth indicators (such as the percentage of S&P 500 stocks trading above their 200-day moving average) actually declined in late September, pointing to a less robust foundation.

- Labor market softness: The surprise decline in private payrolls raised concerns that growth momentum is slowing more quickly than expected. Investors are now balancing the benefits of lower rates against the risk of a weaker economy.

- Credit market stress: While spreads tightened after the Fed cut, elevated issuance in high-yield and municipal markets weighed on valuations, showing that not all fixed-income sectors are benefiting equally from easier policy.

- Seasonal dynamics: Historically, October has been a choppier month for equities. Combined with already stretched positioning, this could make markets more sensitive to surprises.

- Global diversification remains key: International equities continue to provide differentiated opportunities, especially as currency dynamics shift in response to Fed easing.

Economic Backdrop & Key Data

- Labor & employment: The labor market cooled further. Private payrolls fell by 32,000 jobs in September according to ADP—an unexpectedly negative print. This weakness underscored the rationale behind the Fed’s decision and the possibility of further easing.

- Inflation & prices: Inflation remained sticky but stable. The Consumer Price Index (CPI) rose ~2.9% year-over-year in August, with core CPI steady at 3.1%. Meanwhile, the Fed acknowledged inflation “has moved up and remains somewhat elevated.”

- Global growth & PMIs: Purchasing Managers’ Indexes (PMIs) across regions suggest moderate but resilient growth. While the drag from tariffs and global uncertainty persists, expansion is holding. The New York Fed now projects somewhat stronger growth and lower inflation than earlier estimates.

- Monetary policy pivot: The Fed’s 25 bps cut in September was a clear signal that it is shifting toward a more accommodative stance. The FOMC noted that downside risks to employment have increased. In its updated economic projections, the Fed allowed for more easing but remained relatively cautious compared to market expectations.

October Outlook & Key Drivers

Market Risks & Sentiment

Markets enter October in a cautious, “wait-and-see” mode. After strong gains through September, investors are weighing whether current valuations, slower growth, and the Fed’s pacing of policy cuts leave room for further upside.

- Earnings season: Corporate results and forward guidance will be closely watched. Any disappointment could trigger sharp market reactions.

- Valuation concerns: Many market strategists and pundits have noted that U.S. equities now appear overvalued relative to historical metrics. Measures such as the Shiller CAPE ratio and forward Price to Earnings (P/E) multiples are above long-term averages. While accommodative policy and earnings growth support markets, elevated valuations may limit upside and increase sensitivity to economic or earnings surprises.

- Seasonal volatility: October has historically been a choppier month for equities, which could exacerbate near-term swings.

- Credit stress: Elevated issuance and margin pressure in weaker credits or highly leveraged sectors may spread to broader credit markets.

- Growth path: Economic indicators suggest that the U.S. economy is growing, but at a more moderate pace than earlier in the year.

- Consumer spending, while still positive, is showing signs of fatigue after several quarters of above-trend growth. Retail sales and services activity indicate that households may be beginning to tighten budgets in response to higher living costs and lingering tariff effects.

- Manufacturing and industrial demand have softened in recent months. Surveys such as ISM Manufacturing and regional Fed manufacturing indexes point to slower new orders and production. Any further declines could pressure corporate earnings and capital expenditures, feeding back into broader economic growth.

- Inflation dynamics: Sticky inflation remains a risk. If inflation reaccelerates or refuses to decelerate further, the Fed may hesitate on aggressive easing.

- External shocks: Geopolitical events, trade developments, or unexpected commodity price movements could disrupt correlations and amplify volatility.

- Fed & monetary policy: The key question is whether the Fed proceeds with further cuts—or pauses depending on incoming data. Markets currently price in more easing, with the general consensus being two additional 0.25% rate cuts through year end.

Beyond the Markets - Wealth Planning Actions

As the year draws to a close, it is a good time to review your financial position and make adjustments to help protect and optimize your wealth. Paying attention to cash, investments, benefits, and taxes now can help you enter the new year in a strong position.

Review cash holdings

Following the Fed’s rate cut last month, savings accounts and money market yields have generally declined. With additional rate cuts anticipated through year-end and into early 2026, it is important to ensure your cash is still working effectively for you, whether through higher-yield accounts or short-term investments.Review equity exposure

U.S. and international equities have delivered strong returns, averaging more than 20% annually over the past three years. After this period of exceptional performance, your equity allocation may now be overweight relative to your original target. Therefore, it may be a good time to rebalance your portfolio and take some profits. Additionally, investors with a shorter time horizon, such as those approaching retirement, may want to evaluate whether reducing equity exposure aligns with their risk tolerance and specific time horizon.Open enrollment planning

If you are entering your employer’s annual benefits open enrollment period, this is an important opportunity to review and optimize your benefits elections. Employer-provided health insurance premiums are expected to rise between 5% and 10% this year. If you have multiple plan options, it is important to evaluate the total costs—including premiums, deductibles, and out-of-pocket expenses—relative to your anticipated healthcare needs.

For example, a High-Deductible Health Plan (HDHP) may have higher out-of-pocket costs, but its typically lower premiums, combined with the tax advantages of contributions to a Health Savings Account (HSA), may make it a cost-effective choice for individuals with average to above-average health.

Tax minimization strategies

Review your taxable investment accounts to identify potential tax-loss harvesting opportunities. While strong market performance this year may reduce the number of positions eligible for tax-loss harvesting, reviewing your portfolio now may still help to reduce your tax bill.

Consider Qualified Charitable Distributions (QCDs): For individuals age 70½ and older with an IRA, QCDs allow you to donate up to $100,000 per year directly from your IRA to a qualified charity. QCDs count toward your required minimum distribution (RMD) but are excluded from taxable income, potentially lowering your overall tax liability while supporting charitable causes. This can be a strategic way to reduce taxes if you are charitably inclined and have IRA accounts.

Medicare Enrollment

For individuals approaching age 65—or those eligible due to disability—year-end is a key time to review Medicare options. The Initial Enrollment Period begins three months before your 65th birthday and extends three months after, while the Annual Enrollment Period runs from October 15 to December 7 each year.

During this time, you can:

Enroll in Original Medicare (Part A & B) if you haven’t already.

Select a Medicare Advantage (Part C) or Medicare Prescription Drug Plan (Part D) that fits your health needs and budget.

Review supplemental Medigap policies to cover potential gaps in coverage.

Even if you are already enrolled, this period is an opportunity to compare plans, premiums, and provider networks to ensure your coverage remains cost-effective and comprehensive for the coming year. Reviewing your options now helps avoid late-enrollment penalties and ensures your plan aligns with your anticipated healthcare needs.

As always, if you have questions about your year-end planning needs—or if you know someone who could benefit from a review of their portfolio, benefits, or tax strategies—please do not hesitate to contact us. We are here to help ensure financial plans remain aligned with individual goals and circumstances.

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.