October Market & Economic Recap: Fed Cuts, AI Gains, and Navigating Year-End Volatility

October markets were mixed, but posted positive returns overall. U.S. mid- and small-cap stocks softened, while large caps, international stocks, and bonds advanced on strong earnings, lower interest rates, and AI-driven growth.

October Recap

After a strong run through September, markets entered October with a more cautious tone. While U.S. long-term rate expectations softened, underlying breadth and sentiment weakened. Investors grew more selective as valuations stretched and growth expectations moderated.

Economic data was mixed and, in some cases, missing. The ongoing U.S. government shutdown disrupted key reports such as employment and inflation, leaving investors without the usual guidance on growth and price trends. Despite the “data vacuum,” the Federal Reserve and other sources provided enough insight to keep the outlook moderately constructive.

Inflation data for September showed price growth easing slightly, and business surveys reflected modest inflation and wage pressures. The Fed’s Beige Book described economic activity as “little changed” and employment as “stable,” though some softening was noted in consumer spending and hiring.

Global conditions were also mixed. The IMF trimmed its global growth forecast to 3.2% for 2025 and 3.1% for 2026, citing slower trade and lingering geopolitical tensions. Consumer and business confidence slipped modestly, suggesting the economy remains resilient but not exuberant.

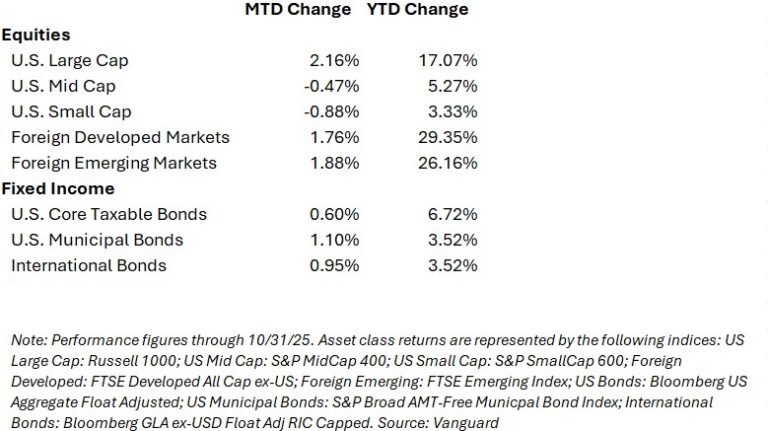

Market Snapshot (through October 31, 2025)

Market Performance & Economic Backdrop

U.S. large cap equities delivered solid gains in October, supported by resilient earnings. By contrast, U.S. mid-cap and small-cap stocks lagged in October, with both categories posting modest declines for the month. U.S. mid-cap stocks declined about 0.5%, while U.S. small cap stocks fell roughly 1%, reflecting investor caution toward economically sensitive segments of the market. Overseas, both developed and emerging market equities finished positive for the month.

In fixed income, U.S. investment-grade bonds provided steady returns with tight credit spreads and attractive coupon income. High-yield corporate bonds continued to perform well, supported by resilient earnings and compressed spreads, while international and emerging market debt benefited from declining U.S. Treasury yields, though volatility remained elevated. Overall, diversification across equity and fixed-income segments remains key, with portfolios positioned to balance growth opportunities, yield, and risk management.

Earnings and Valuations

Corporate earnings growth has been stronger than many analysts expected, led by technology and industrial companies. However, valuations in parts of the market have become elevated. Investors are increasingly differentiating between companies with genuine earnings momentum and those priced primarily on optimism. A more selective environment is emerging, where fundamentals are likely to matter more than macro narratives.

Interest Rates and Inflation Trends

In October, the Federal Reserve delivered its second consecutive rate cut, following the initial 25 basis point reduction in September. This move lowered the target range for the federal funds rate to 3.75%–4.00%, marking the Fed’s continued shift toward a more accommodative stance in response to moderating inflation and signs of slower economic growth. The back-to-back cuts reflect the Fed’s focus on supporting the economy while carefully monitoring labor market conditions and price pressures, signaling to markets that policy is now aimed at sustaining growth without stoking renewed inflation.

Economic Growth

One of the most notable economic stories this year has been the rapid buildout of artificial intelligence (AI) infrastructure and its broad impact across industries. Companies are investing heavily in data centers, semiconductors, and software

designed to integrate AI into business operations.

AI adoption is beginning to lift productivity in sectors ranging from logistics and manufacturing to financial services and healthcare. This could help offset the drag from slower labor-force growth and keep the economy’s long-term growth

potential intact. At the same time, the surge in AI-related investment has driven strong corporate spending and supported demand for technology and industrial equipment.

However, not all effects are positive. The expansion of data centers has contributed to rising energy consumption and

power grid strain in certain regions. Additionally, the concentration of market gains among a handful of AI-focused companies has increased valuation and diversification risks for investors. While AI is likely to remain a powerful growth engine, it is important to balance enthusiasm with discipline—focusing on long-term opportunities rather than short-term market momentum.

Looking Ahead: November & Beyond

As we move into the final stretch of 2025, several themes stand out:

- Data releases may be delayed or volatile once the government reopens, making markets more reactive to surprises.

- The Federal Reserve remains in focus as investors debate whether additional rate cuts are coming before year-end.

- Corporate earnings reports will influence whether equity valuations are justified or stretched.

- Seasonal volatility tends to pick up in the fourth quarter, though historically, markets often finish the year stronger after brief October pullbacks.

- Geopolitical tensions, trade developments, and fiscal uncertainty remain potential swing factors for risk assets.

- For fixed-income investors, yields remain attractive, though high-yield and credit sectors could face pressure if economic data deteriorates.

Many leading strategists are urging caution ahead of potential market turbulence. Goldman Sachs’ David Solomon warned this week that a pullback of 10%–20% in equities within the next 12-24 months is a realistic scenario, even in the absence of a major macro shock. Likewise, Morgan Stanley’s Ted Pick described a 10%–15% correction as “healthy” and somewhat routine in a longer-term bull market. While these forecasts are not predictions of a severe correction, they point to elevated valuations and concentrated markets, signaling that volatility may increase in the months ahead.

In short, expect choppy but opportunity-filled markets into year-end, with the potential for volatility around key economic data and Fed meetings.

Closing Thoughts & Year-End Planning

As 2025 winds down, the financial landscape remains balanced between opportunity and caution. Economic growth continues, but at a slower pace; inflation is moderating, but not gone; and policy remains supportive, but uncertain.

With strong market performance over the past three years, now may be a good time to review your investment accounts to ensure your portfolio risk still aligns with your personal risk tolerance and your remaining time horizon for your investment goals. As a general guideline, if an investment allocation drifts more than 5% from its target, it may signal that a rebalance is warranted to keep your strategy on track.

For investors holding actively managed stock funds in taxable accounts, December may bring larger capital gains distributions after several years of strong performance. Most fund families announce projected distributions in November, so it is important to factor these into your tax planning—especially if you pay quarterly estimated taxes. For actively managed funds in particular, be mindful of “buying the distribution,” which can result in unnecessary or even significant added tax costs.

For those nearing or in retirement, the focus remains on three priorities: maintaining sufficient liquidity for spending needs, ensuring portfolio risk aligns with long-term goals, and preserving tax efficiency.

As always, please reach out if you would like to discuss your portfolio positioning, tax strategies, or broader financial plan.

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.