November Market & Economic Recap: Balancing Growth and Stability as the Fed Weighs Its Next Move

From equities to bonds, we break down last month’s market performance and key considerations for year-end planning.

November Recap

November 2025 was marked by heightened investor attention on the Federal Reserve and the potential for a policy pivot. Throughout the month, markets increasingly priced in a rate cut at the Fed’s December meeting, with analysts estimating an 80–85% chance of a 25-basis-point reduction. Dovish commentary from several Fed officials reinforced this expectation, helping to lift equities at various points during the month. However, the Fed’s path remains uncertain, as mixed economic data and the presence of more hawkish voices within the committee continue to complicate the outlook.

Economic Indicators & Labor Market Trends

Economic indicators in the U.S. presented a mixed picture. The Fed’s Beige Book reported largely flat economic activity, with about half of the regional districts noting softer employment and weaker consumer spending, signaling a gradual cooling of the labor market. At the same time, inflation continued to erode real income gains, constraining consumer spending, particularly as the holiday season approached. Manufacturing activity also softened, with slowing new orders and increasing inventories suggesting weaker demand or elevated costs. Collectively, these trends underscore that while the economy is not in contraction, growth is decelerating.

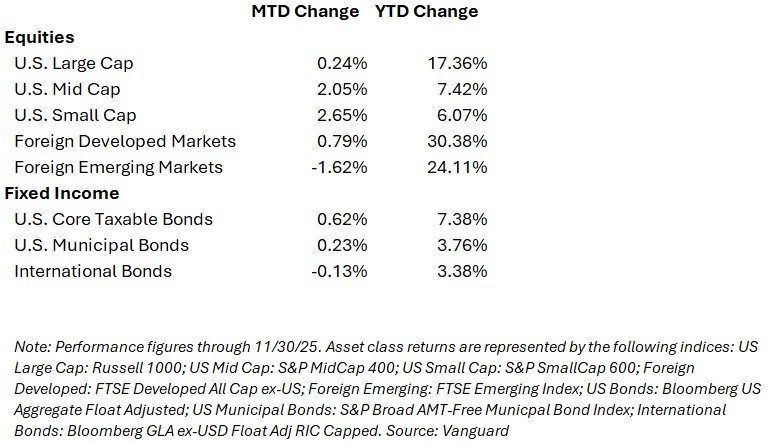

Market Snapshot (through November 30, 2025)

Market Performance & Economic Backdrop

Equities

U.S. equities delivered broadly positive results in November, with performance strongest among smaller-capitalization stocks. Large caps posted a modest 0.24% gain, while mid-caps and small-caps outperformed, rising 2.05% and 2.65%, respectively. Strength in these higher-beta segments reflects improving sentiment around a potential Federal Reserve policy shift and growing optimism that economic conditions may be stabilizing. Foreign developed markets also advanced (+0.79%), while emerging markets declined (-1.62%) amid continued country-specific and geopolitical pressures.

Fixed Income

November was a favorable month for fixed-income investors. The broader U.S. bond market (as measured by the Bloomberg US Aggregate Bond Index) generated a positive return of roughly +0.6% as yields declined modestly. The yield on the 10-year Treasury note dipped to around 4.00%, reflecting renewed investor conviction that the Fed will cut interest rates at its December meeting. Corporate bonds and high-yield debt underperformed slightly relative to government bonds but still provided modest positive carry as credit spreads remained stable.

Altogether, November’s backdrop reinforced the value of a balanced portfolio. For investors focused on income or capital preservation — particularly those nearing or in retirement — the rally in the bond market and modest equity gains illustrate why a diversified allocation remains appealing in a period of policy uncertainty and economic transition.

Global Economic Backdrop

Globally, central banks appear to be approaching the end of the ultra-loose monetary policy cycle. Investors are increasingly weighing the impact of shifting policy regimes on global growth. While some major economies—including China—saw modest upward revisions in GDP forecasts, overall global economic growth remains uneven. This combination of slowing U.S. activity, selective global strength, and policy uncertainty creates a nuanced backdrop for investors.

Looking Ahead: December & Year-End Considerations

As we head into December, several market and economic events deserve attention. The Federal Reserve’s December 9–10 meeting will likely dominate market focus, as investors look for updated guidance on interest rates and the broader economic outlook. December also marks the formal end of the Fed’s balance-sheet reduction program, a structural shift that could influence liquidity and longer-term bond yields. Key economic data—covering inflation, jobs, manufacturing and services activity, retail spending, and GDP—will help clarify the economy’s momentum as the year wraps up.

It has also been a constructive year across many major asset classes, with both equities and fixed income posting broad gains in the U.S. and internationally. This has provided a supportive backdrop for investors who maintain well-diversified portfolios, as strength across multiple areas of the markets has helped smooth out volatility and contribute to more consistent overall returns.

Seasonal patterns—including holiday-related shifts in consumer spending, lighter trading volumes, and typical year-end portfolio adjustments—may introduce some short-term noise, but these developments will help shape market dynamics as 2025 concludes and set the stage for early 2026.

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.