May Market Recap and June Outlook: Ongoing Trade Uncertainty

In May, markets showed resilience despite mixed economic signals, including slower growth projections, persistent inflation concerns, and rising U.S. debt levels. While the OECD lowered its U.S. GDP forecast to 1.6%, equities—particularly tech—rebounded strongly, and international equity markets continued with strong performance. Bond markets faced pressure as Treasury yields climbed above 4.5%, reflecting fiscal concerns and waning foreign demand. As investors look ahead to key June events, including a Fed meeting and CPI report, Overture Wealth Management remains focused on diversified, long-term strategies to navigate ongoing uncertainty.

Market & Economic Recap – May 2025

May brought a mix of caution and resilience in U.S. markets, as economic signals remained mixed and investors weighed the impact of tariffs, inflation, and central bank policy.

Growth Forecasts Lowered

The OECD revised its U.S. GDP forecast for 2025 down to 1.6%, compared to 2.8% in 2024. The downgrade reflects mounting trade frictions and slowing global demand—more a sign of cooling momentum than an impending recession.

Inflation & the Fed

The Consumer Price Index for All Urban Consumers (CPI-U) rose by 0.2% in April, according to data released in May. The Federal Reserve has maintained a “wait and see” approach, closely monitoring wage growth and global uncertainties before making any decisions on potential rate cuts. However, concerns persist that inflation could rise later in the year due to delayed effects from recently implemented tariffs.

Equity Markets Show Resilience

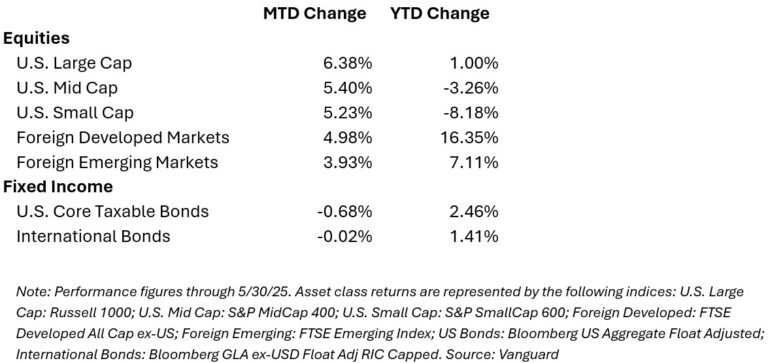

Despite macroeconomic headwinds, U.S. equity markets remained steady:

- The S&P 500 continued to recover from losses experienced from February to early April and moved into slightly positive territory for the year

- International equities also finished the month with positive performance and continue to significantly outperform U.S. equities year-to-date.

- The Nasdaq led gains, driven by strong AI and semiconductor earnings. The tech benchmark finished up about 10% for the month.

Bond Markets Experienced Price Declines

Bond markets remained relatively rangebound in May, reflecting a market caught between persistent inflation and uncertain monetary policy.

- Bond markets remained rangebound, as investors tracked inflation and Fed signals.

- U.S. Treasury Yields: The 10-year U.S. Treasury yield surged above 4.5%, reflecting concerns over fiscal deficits and the potential impact of new tariffs. This increase in yields has led to heightened investor caution and a reevaluation of bond market dynamics.

- Investor Sentiment: Global investors are becoming increasingly wary of U.S. government debt. Factors such as diminishing returns and rising currency-hedging costs have made domestic bonds in other countries more attractive, leading to a shift in capital away from U.S. assets.

What to Watch – June 2025

- Federal Reserve Meeting (Mid-June)

Markets are not anticipating a rate cut this month, but the Fed’s guidance could shape expectations for later this year. - CPI Report (June 12)

The upcoming Consumer Price Index (CPI) reading will be closely watched. Softer inflation could open the door to policy easing later this summer. - Q1 Earnings Wrap-Up

Earnings season is nearly complete, with many companies—particularly in tech, energy, and industrials—demonstrating resilience despite uncertainty. - S. Election Season Begins to Weigh on Markets

With November elections approaching, investors are beginning to assess potential impacts on trade, taxation, and regulation.

Global Snapshot: May Recap & June Outlook

May Highlights:

- Global growth forecasts were lowered to 2.9%, primarily due to tariff-related trade slowdowns.

- Latin America remained steady, while Asia saw weaker factory output.

Looking Ahead in June:

- Europe: The ECB cut rates by 0.25% but hinted at a pause in its year-long easing cycle after inflation returned to its 2% target.

- China: Anticipated economic stimulus may aim to offset sluggish manufacturing.

- Geopolitical Risks: Markets are watching global trade talks and energy prices, especially in the Middle East and Eastern Europe.

Market Snapshot (through May 30, 2025)

U.S. Treasury Debt Concerns

Concerns about the U.S. national debt continued in May as Treasury borrowing levels continued to climb. Total federal debt surpassed $36 trillion, prompting renewed scrutiny from economists, rating agencies, and global investors.

Several key issues are drawing attention:

- Rising Interest Costs: With short-term rates still elevated, the cost of servicing debt has ballooned. Interest payments now account for a growing share of the federal budget, potentially crowding out other priorities.

- Investor Appetite: Investor demand for Treasuries has not meaningfully shifted, but recent auctions have shown signs of softening interest from foreign buyers—particularly amid global uncertainty and higher yields in competing markets.

- Credit Rating Watch: While the U.S. retains a high credit rating, both Fitch and Moody’s have warned that sustained fiscal deficits and political gridlock could eventually trigger further downgrades.

Looking ahead, market participants will be watching the upcoming federal budget debates and long-term deficit projections. While the U.S. remains one of the world’s most stable issuers, growing debt levels could influence future tax policy, monetary policy, and bond market dynamics.

Portfolio Perspective

Markets continue to digest shifting inflation trends, central bank decisions, and geopolitical dynamics. Overture’s current portfolio allocations continue to maintain tactical exposures to sub-asset classes that can help to hedge against inflation. In times like these, we stay focused on what we can control:

- Customized portfolios designed with your particular goals, time horizon and risk tolerance in mind

- Diversification across asset classes and regions

- Disciplined rebalancing aligned with your financial goals

Remaining committed to a long-term plan helps navigate short-term uncertainty and stay on track for future success.

Plan Ahead

As we approach the middle of the year, it’s a good time to review your estimated tax payments, if applicable. If you’re self-employed, receive investment income, or have limited withholding, keep in mind:

- The next quarterly estimated tax deadline is June 17, 2025

- Missing this deadline could result in IRS penalties or interest charges

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.