June Market Recap and July Outlook: Ongoing Trade Uncertainty

Markets demonstrated resilience in June, even as uncertainty around Federal Reserve policy and mixed economic data persisted. The S&P 500 posted strong gains, buoyed by continued strength in the technology and healthcare sectors. Inflation came in slightly below expectations, which reinforced market optimism around potential interest rate cuts later this year. However, the Fed maintained its cautious stance, opting to keep rates unchanged in June.

President Trump has continued to publicly pressure Fed Chair Jerome Powell to reduce interest rates more aggressively, even suggesting he may replace Powell if the pace of policy change does not align with the administration’s goals. These dynamics have introduced another layer of uncertainty to monetary policy and could influence the economic backdrop as we head into the fall.

In the bond market, yields declined modestly during the month, offering some relief and stability for conservative portfolios. On the consumer side, spending has remained relatively strong, though early signs of cooling are emerging in the housing and travel sectors.

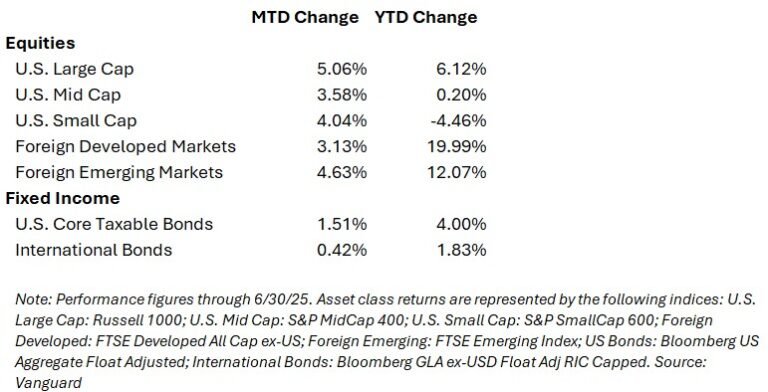

Market Snapshot (through June 30, 2025)

Looking Ahead to July

The month of July will center around inflation data and the kickoff of corporate earnings season. Investors will be watching closely for guidance on how companies are managing input costs and consumer demand, particularly as signs of a potential economic slowdown begin to surface. Any downward revisions in earnings or cautious corporate outlooks could lead to short-term volatility. As always, we continue to advocate for a long-term, diversified investment approach that’s grounded in your personal financial goals.

Trade & Tariff Update

Trade policy remains a key issue this summer as President Trump’s July 9 deadline for a new wave of tariffs approaches. Initially imposed in April and paused for 90 days, the proposed tariffs—some reaching 30–35%—are part of a broader push for what the administration calls “reciprocal trade.” Several major trading partners, including India, Japan, the U.K., and the EU, are actively negotiating to avoid the hikes. While deals with India and the U.K. appear within reach, talks with Japan and the EU remain tense—particularly on issues related to autos and steel. A limited agreement with China has already been reached, stabilizing tariffs on rare earth exports. The administration has suggested that up to a dozen new trade deals may be finalized by Labor Day. However, the upcoming July 9 deadline could still be a flashpoint for markets if major agreements remain unresolved.

Legislative Spotlight: Trump’s “Big Beautiful” Tax Bill Advances

On July 1, the Senate narrowly approved President Trump’s highly anticipated tax proposal—formally known as the “One Big Beautiful Bill Act”—by a 51–50 vote, with Vice President Vance casting the deciding ballot. The bill would permanently extend the 2017 tax cuts and introduce new deductions for tips, overtime pay, auto loan interest, and state and local taxes (SALT). It also increases federal spending on defense and border security.

To offset the cost, the legislation proposes deep cuts to Medicaid, food assistance, and green energy programs. Analysts estimate it could add roughly $3.3 trillion to the national debt over the next decade and potentially result in up to 12 million Americans losing health coverage due to Medicaid reductions.

The bill is now back in the House, where further negotiations are ongoing. While House leadership is working to unify support behind the Senate’s version, objections from conservative lawmakers over the entitlement cuts could delay final passage. President Trump has urged swift action, pushing for the bill to be on his desk by July 4 as a cornerstone of his economic platform.

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.