July Market Recap and August Outlook: Continued Strong Equity Performance

Despite a steady stream of political noise, geopolitical risks, and mixed economic signals, markets remained largely unshaken in July. Even with persistent uncertainty about the direction of fiscal policy, international tensions simmering in the background, and President Trump’s posturing for an early replacement of the Federal Reserve Chair, Jerome Powell, investor confidence remained largely intact.

In fact, July reminded us again that markets are not the economy—and certainly not the headlines. Equity indexes climbed steadily, credit spreads remained tight, and inflation data continued to move in the right direction. Strong corporate earnings were the real story of the month, offsetting concerns about slower growth and a still-hawkish Fed.

The Data

- Inflation continues to cool.

The Consumer Price Index (CPI) rose just 0.3% in June (per CPI-U data released on July 15th), bringing the annual inflation rate to 2.7%, the lowest since early 2021. Core CPI (excluding food and energy) increased 0.2% month-over-month and 2.9% year-over-year.

Source: U.S. Bureau of Labor Statistics, August 2025

- Labor market remains strong but softening.

The U.S. added a modest 73,000 jobs in July per the non-farm payroll report. The unemployment rate came in at 4.2%. The unemployment rate has remained in a narrow range of 4.0% – 4.2% since May 2024. The Bureau of Labor Statistics (BLS) revised downward the payroll growth numbers for May and June by a combined 258,000, the largest two-month revision ever outside of a recession. The massive downward revision led President Trump to fire the head of the BLS on August 1st.

Source: U.S. Bureau of Labor Statistics, USA Today

- Fed policy remains in focus.

The Federal Reserve left rates unchanged at its late July meeting, but signaled that it remains data-dependent. Futures markets are now pricing in a potential rate cut of up to 1/2 percent as early as September, contingent on further softening in core inflation.

Source: CME FedWatch Tool

- Consumer confidence improves slightly.

Consumer Confidence ticked up modestly in July, with the Consumer Confidence Index reaching 97.2, up 2.0 points from 95.2 in June. The Present Situation Index dipped 1.5 points to 131.5, while the Expectations Index rose 4.5 points to 74.4, remaining below the recession‑warning level of 80 despite slight improvement. Source: The Conference Board

Markets in July

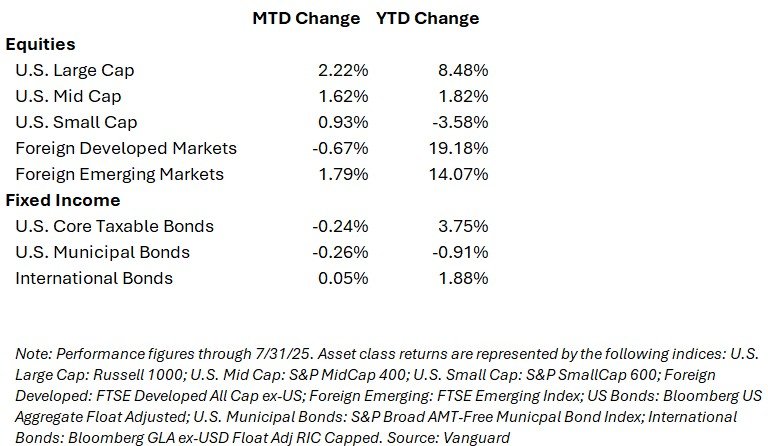

U.S. and Emerging market equities posted solid monthly returns, while Foreign Developed Markets experienced a slight pull back. U.S. investment-grade fixed income investments were slightly negative for the month, while international investment grade bonds were relatively flat.

Market Snapshot (through July 31, 2025)

Looking Ahead to August

August tends to be a seasonally quieter month for trading volume, but the economic calendar is full. Key events on the horizon include:

- July CPI and PPI reports (August 12–14)

- Jackson Hole Economic Symposium (August 21–23)

- Continued Q2 earnings season, particularly in retail and tech

Investors should be prepared for more sideways market movement, potential sector rotation, and increasing policy clarity—especially as the fiscal outlook for 2026 begins to take shape.

Beyond the Markets – Personal Planning Actions

Maximize Tax Benefits Under the One Big Beautiful Bill Act

The recently enacted One Big Beautiful Bill Act introduces several tax provisions that can benefit individuals, particularly seniors and those in high-tax states. Consider the following strategies:

- Leverage Enhanced Senior Deductions: If you’re 65 or older with an adjusted gross income (AGI) under $75,000 (or $150,000 for married couples), you may qualify for an additional $6,000 (single) or $12,000 (married) deduction on your federal income taxes for 2025 through 2028. This enhanced deduction may allow for additional creative tax planning around things such as Roth conversion strategies, or realized capital gains.

- Evaluate State and Local Tax (SALT) Deductions: For households earning under $500,000, the SALT deduction cap has been temporarily increased to $40,000 through 2029. This change may make itemizing deductions more advantageous, especially in states with high local taxes. Investopedia

- Consider Charitable Giving Strategies: The act allows for charitable contributions up to $2,000 for married couples ($1,000 for others) without itemizing deductions. This provision can simplify your giving strategy while still providing tax benefits.

- New Car Loan Interest Deduction: Effective in 2025 through 2028, you may deduct up to $10,000 per year in car loan interest, for vehicles purchased after 12/31/24 and provided the vehicle undergoes final assembly in the U.S. This deduction phases out for borrowers with modified adjusted gross income over $100,000 ($200,000 for joint filers).

These provisions offer opportunities to reduce your tax liability and enhance your financial planning. Consulting with a tax professional and financial advisor can help you navigate these changes and implement strategies that align with your financial goals.

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.