December Market & Economic Recap: From Anticipation to Transition

Markets close out the year focused on policy normalization, cooling growth, and opportunities heading into 2026.

December Recap

December 2025 marked a transition month for markets, as much of the policy uncertainty that dominated late 2025 gave way to clearer direction from the Federal Reserve. Following the Fed’s initial rate cut earlier in the fall, December’s meeting reinforced the view that inflation is trending lower and economic growth is slowing toward a more sustainable pace.

While no major policy surprise emerged, markets spent much of December digesting what comes next. Fed officials emphasized a data-dependent approach going forward, tempering expectations for rapid or aggressive easing in 2026. As a result, risk assets experienced more muted and uneven performance than earlier in the quarter, with investors increasingly differentiating between sectors and asset classes rather than bidding up markets broadly.

Economic Indicators & Labor Market Trends

Economic data released in December reinforced the theme of gradual cooling rather than abrupt slowdown. Labor market indicators continued to soften at the margin, with job growth moderating and wage pressures easing, though unemployment remains historically low. Consumer spending showed signs of resilience into the holiday season, but higher borrowing costs and lingering inflation pressures continue to weigh on discretionary spending.

Inflation data remained on a favorable trajectory, particularly in goods and housing-related components, giving policymakers more confidence that restrictive policy is no longer necessary. At the same time, manufacturing activity stayed subdued, while services remained more stable — a pattern consistent with a late-cycle economy adjusting to tighter financial conditions.

Overall, the December data suggest an economy that is slowing, but still expanding — a constructive backdrop as markets enter 2026.

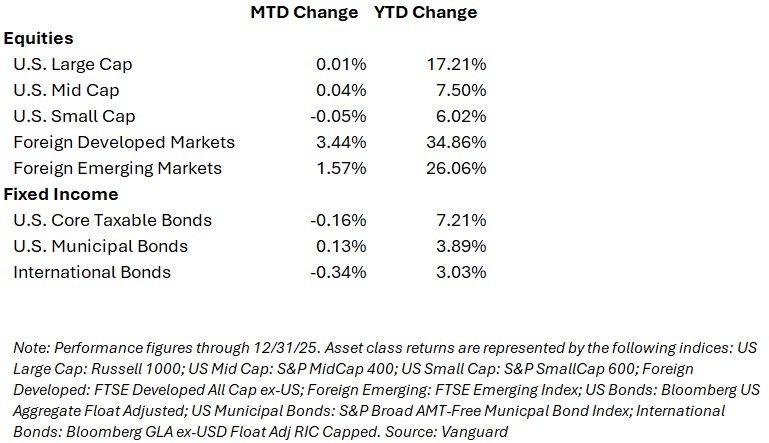

Market Snapshot (through December 31, 2025)

Market Performance & Economic Backdrop

Equities

Equity markets finished December with more modest and mixed results compared to the strong gains seen earlier in the quarter. Large-cap U.S. stocks were relatively flat for the month, while smaller-cap and more economically sensitive areas gave back some of their recent outperformance as investors reassessed growth expectations for 2026. In contrast, international developed markets and emerging market equities posted stronger gains, benefiting from currency movements, improving global growth expectations, and shifting interest-rate dynamics outside the U.S.

Despite the quieter finish for U.S. equities, markets ended 2025 with solid gains overall, supported by improving earnings expectations and growing confidence that monetary policy is transitioning from a headwind to a potential tailwind.

Fixed Income

Fixed income remained a bright spot in December. Bond yields generally drifted lower following the Fed’s rate cut, supporting positive returns across much of the bond market. High-quality government and investment-grade bonds benefited most, while credit-oriented sectors delivered steady income with limited spread volatility.

For investors focused on income, capital preservation, or portfolio stability — particularly those nearing or in retirement — 2025 marked an important reset. Bonds once again offered meaningful yield and diversification benefits after several challenging years.

Global Economic Backdrop

Globally, central banks appear to be moving in the same general direction, though at different speeds. Several developed economies are further along in the easing cycle, while others remain cautious due to lingering inflation risks. Growth abroad remains uneven, with pockets of resilience offset by structural challenges in certain regions.

This divergence reinforces the importance of global diversification, as returns are increasingly driven by local economic conditions and policy decisions rather than broad, synchronized cycles.

Looking Ahead: January 2026 and the Year Ahead

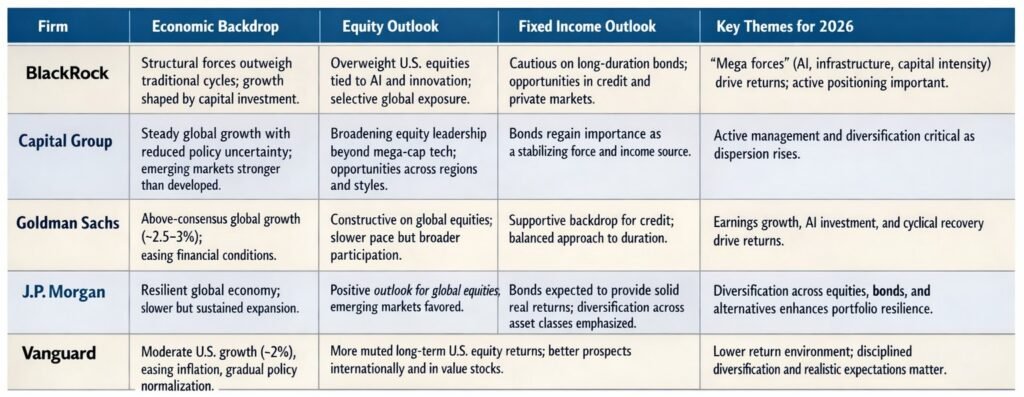

As we look ahead to 2026, many leading market strategists broadly share a constructive — though more measured — outlook for markets and the economy. The common theme across many of the outlooks is that the global economy is expected to continue expanding, inflation pressures are easing, and financial markets are entering a more balanced phase after several years of unusual volatility and concentration.

Economic growth is expected to moderate but remain positive.

Most major forecasters anticipate steady, mid-cycle-like growth rather than recession. U.S. economic growth is generally expected to settle around the 2% range, supported by resilient consumer demand, continued investment in productivity-enhancing technologies, and gradually easing financial conditions. Globally, growth is expected to be uneven but stable, with emerging markets growing faster than developed economies.

Monetary policy is shifting from a headwind to a tailwind.

With inflation continuing to cool, central banks — including the Federal Reserve — are expected to move further into an easing phase in 2026. While most firms do not expect rapid or aggressive rate cuts, the transition away from restrictive policy should provide a more supportive backdrop for both equities and fixed income. Importantly, interest rates are expected to remain higher than pre-pandemic norms, reinforcing the return potential of income-oriented investments.

Equity returns may be more moderate — but more broadly driven.

Across firms, there is consensus that equity returns in 2026 are likely to be lower than the outsized gains seen in recent years, particularly in segments that have benefited from elevated valuations. However, this does not imply a negative outlook. Instead, leadership is expected to broaden beyond a narrow group of mega-cap stocks. International developed markets, value-oriented equities, and more cyclical areas of the market are widely viewed as increasingly attractive as earnings growth becomes a more important driver of returns.

Fixed income is once again a core portfolio building block.

Perhaps the clearest area of agreement is the renewed role of bonds. With yields still elevated by historical standards and inflation moderating, high-quality fixed income is expected to deliver meaningful income and diversification benefits in 2026. Several firms highlight that bonds are now positioned to contribute positively to total returns while also helping to manage portfolio volatility — a notable shift from much of the prior decade.

Diversification and discipline matter more than forecasts.

While outlooks vary on the precise magnitude of returns, the strategic guidance is consistent: diversified portfolios are better positioned in a world of slower growth, normalizing inflation, and divergent regional outcomes. After a strong year across many asset classes, firms also emphasize the importance of disciplined rebalancing, tax awareness, and maintaining alignment with long-term goals rather than reacting to short-term market narratives.

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.