August Market & Economic Recap: Small Caps Lead the Charge

August delivered another month of positive returns across most major asset classes, with equities leading the way as investors positioned for a potential shift in monetary policy. Despite ongoing trade tensions and a mixed economic backdrop, markets rallied on rising expectations of Federal Reserve rate cuts and signs of easing global tariff pressures.

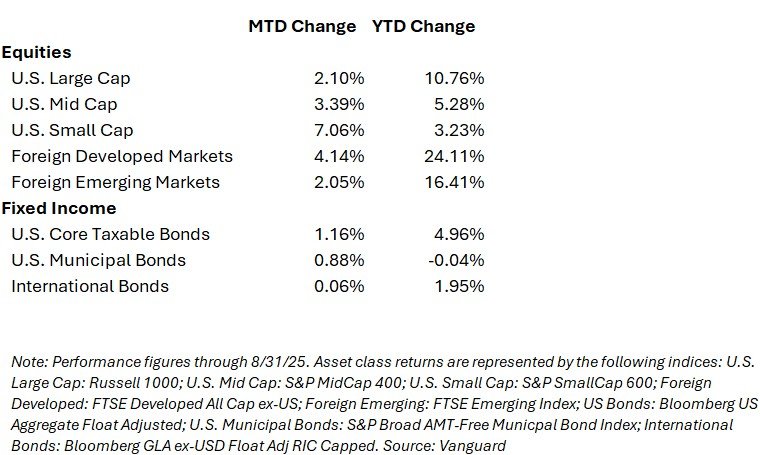

Market Performance

Equities – U.S. & Global

U.S. equities advanced in August, with the S&P 500 gaining roughly 2.0% and closing at a new all-time high of 6,501.86 on August 28. Small-cap stocks outpaced their larger peers with a 7.0% gain for the month, buoyed by improving economic data and growing confidence that the Fed will begin easing policy in September.

International equity markets also participated in the rally. Developed market equities increased by 4.0% for the month, while emerging markets rose by 2.0%.

Fixed Income Markets

Bonds posted modest gains in August as investors positioned for a more accommodative Federal Reserve stance. U.S. Treasuries advanced about 0.9%, supported by dovish remarks from Chair Powell at Jackson Hole and growing market confidence in a September rate cut. Core taxable bonds gained 1.16%, while municipal bonds rose 0.88%, reflecting steady demand from income-focused investors. International bonds were largely flat (+0.06%) as global central banks maintained a cautious approach. Overall, falling rate expectations provided a tailwind across most segments of the fixed income market.

Market Snapshot (through August 31, 2025)

Notable themes:

- Small-caps

led the pack in August, reflecting a renewed appetite for risk and the

prospect of policy easing.

- Foreign

markets, particularly developed economies, continued to outperform on a

year-to-date basis.

- Fixed

income delivered positive returns, supported by falling yield

expectations.

Economic Backdrop

Economic data in August was mixed, reflecting both ongoing pressures and signs of moderation in monetary policy:

- Inflation: Core PCE inflation inched higher, from 2.77% Year over Year to 2.88%, and from 3.20% to 3.33% Month over Month annualized, indicating persistent but moderate price pressures.

- Tariffs & consumer strain: The Fed’s Beige Book reported that rising tariffs weighed on hiring and consumer spending, with households beginning to tighten budgets.

- Policy expectations: Market-implied odds of a September rate cut rose to nearly 96%, with Fed Governor Waller publicly endorsing a series of cuts targeting a neutral rate near 3%.

- Growth outlook: The IMF slightly raised its 2025 U.S. GDP forecast to 1.9% (+0.1%), citing improving trade conditions and supportive market trends, suggesting that growth may be slowing less sharply than previously expected.

September Outlook & Key Drivers

Looking ahead, markets remain focused on central bank actions and evolving global trade conditions.

Macro & Policy Expectations

- Federal Reserve: A widely expected September rate cut is the key focus, driven by cooling labor and inflation trends.

- Global central banks: The ECB remains steady, emphasizing medium-term inflation control, while the Bank of England contends with elevated long-bond yields and structural pressures.

- IMF & global growth: U.S. growth forecasts have been revised higher, while global growth is slowing but proving resilient.

Market Sentiment & Risks

- Equities: Small-caps could see a pause or mild pullback if rate-cut expectations shift, while foreign equities remain attractive if trade tensions stay contained.

- Fixed income: August’s bond rally may moderate, though rate-cut prospects still provide a tailwind. Long-term yields, particularly in the U.S. and U.K., remain a watchpoint.

Investor Confidence

Markets enter September in “wait-and-see” mode ahead of key Fed decisions and economic releases. Business sentiment shows underlying resilience, and a gradual recovery in global GDP growth through 2026 remains plausible.

Key Takeaways

- Monetary policy will drive the narrative: Dovish surprises could lift both equities and bonds, while hawkish signals may trigger volatility.

- Small-caps remain a high-beta trade: Attractive in easing cycles but more sensitive to macro data swings.

- International equities are compelling: Valuations remain reasonable, and cyclical improvement may support continued strength, especially if trade conditions improve.

- Diversification remains prudent: A balanced approach across sectors, geographies, and asset classes can help manage risk in a shifting policy landscape.

Beyond the Markets - Personal Planning Actions

As summer winds down and the final quarter approaches, here are a few timely financial housekeeping steps to consider this month:

- Quarterly Estimated Taxes: If you make estimated tax payments, remember the third-quarter payment deadline is September 15. This is especially important for those with substantial non-wage income, such as business owners, retirees with investment income, or those realizing capital gains.

- Revisit Withholding Elections: With updated income expectations or mid-year bonuses, now is a good time to check your payroll withholdings to help avoid surprises at tax time.

- Review Cash Holdings Ahead of Potential Rate Cuts: With the Federal Reserve widely expected to begin cutting rates in September, now is an opportune time to assess cash positions. Consider whether excess cash could be better deployed—either by locking in higher-yield instruments before cuts occur or by reallocating a portion into investment or debt-reduction strategies.

- Flexible Spending Account (FSA) Usage: If you participate in an FSA, review your balance and plan eligible expenses before year-end deadlines.

DISCLOSURE

Overture Wealth Management LLC (OWM) is a registered investment advisor offering advisory services in the Commonwealth of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Overture Wealth Management LLC (referred to as “OWM”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute OWM’s judgement as of the date of this communication and are subject to change without notice. OWM does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall OWM be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if OWM or a OWM authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.